U.S. Energy Department Announces $1.9 Billion for Grid Upgrades

Related Research

Welcome back to EnerKnol Pulse. This week's roundup includes FERC's new tax regime for partnership pipelines, New York's $1.4-billion renewable spending spree and a sure-to-be controversial emergency plan by PJM. Made possible by the EnerKnol platform. We welcome your feedback at research@enerknol.com

March 19, 2018

Greening Energy Mix

Evolving Power Markets

Developing the Grid

Fossil Fuels & Nuclear

AEP

Calpine

Consumers Energy

Dayton Power & Light

Energy Transfer Partners

Eversource

ISO New England

Jersey Central P&L

MISO

National Grid

Nevada Hydro

PJM Interconnection

Public Citizen

SCE

Sunoco Pipeline

PJM Interconnection LLC unveiled a suite of recommendations to bolster the resiliency of the bulk power system, responding to an inquiry by the Federal Energy Regulatory Commission. PJM proposed that it make out-of-market payments to generators in times of emergencies and prolonged degraded operations. It asked FERC to strengthen rules for coordination between grid managers and pipeline operators and develop processes for identifying vulnerabilities, assessing threats and system restoration. Since the Polar Vortex in 2014 caused major disruptions to the power system, U.S. regulators and grid operators have scrambled to harden the transmission network and generator fleet through a number of rules and compensation schemes.

New York Gov. Andrew Cuomo, a Democrat, announced that 22 utility-scale solar farms, three wind farms and one hydroelectric project won contracts to supply renewable energy in the first solicitation under the state’s Clean Energy Standard, according to a March 8 press release. The projects will add over 1,380 megawatts of capacity, or enough power to meet the energy needs of nearly half a million homes, putting the state closer to meeting its goal to source half its electricity supplies from renewable sources by 2030. The New York State Energy Research and Development Authority, known as NYSERDA, will issue the next solicitation for large-scale renewable energy on April 25. Cuomo also announced that the state has formally requested an exclusion from the federal government’s five-year oil and gas program that proposed to open over 90 percent of the total U.S. offshore acreage to drilling.

Nevada Hydro Company Inc. asked the Federal Energy Regulatory Commission for authorization to charge cost-based rates and gain recognition as a wholesale transmission facility for its proposed Lake Elsinore Pumped Storage project, as it seeks to continue the development process and participate in the state’s grid plans, according to a March 9 petition with the agency. The commission had previously found that the project wasn’t eligible for the rates due to the California grid operator’s involvement in the project’s operations, but has since issued a change in policy. Nevada Hydro seeks to start the 500-megawatt project, located in Riverside County, Calif., by early 2023.

The Hawaii legislature passed a measure that would create a three-year pilot rebate program to incentivize the installation of energy storage systems paired with solar panels for low- and middle-income residents. The bill also sets up a rebate program aimed at expanding the adoption of renewable energy and energy efficiency among residents. State lawmakers have aggressively sought to pass measures to harness the island’s wind and solar energy in a bid to lower what are some of the most expensive electricity and fuel prices in the nation. (HB 1593)

The New York House passed legislation on March 12 that would set a goal of achieving a 100 percent reduction in greenhouse gas emissions relative to 1990 levels, with an interim cut of 50 percent by 2030. The bill calls for regulatory measures to achieve the goal, including performance standards for emitting sources, a market-based price on carbon, and a shift to renewable energy and energy efficiency from fossil-fueled power. (A 8270B)

The Hawaii legislature on March 14 passed a bill that would establish a goal to cut and ultimately eliminate the use of fossil fuels for ground transportation in three decades, including through the expansion of charging stations and other infrastructure to spur the adoption of electric vehicles. The measure also sets a new benchmark for the reduction of fossil fuel use in transportation for five years from the previous target. The island chain aims to source all of its electricity from renewables by 2045. (HB 1580)

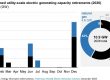

Wind and solar were the only types of new generation placed into service in January, totalling 1,586 megawatts of capacity, or about the same as a year ago, while added capacity from natural gas and nuclear fell to zero, according to data from the Federal Energy Regulatory Commission. Renewable energy sources, which includes biomass, geothermal, hydropower, solar, and wind, now account for one-fifth or 20 percent of total available U.S. generating capacity. Federal and state incentives and falling costs have spurred rapid growth of renewables.

A revamp of ISO New England Inc.’s annual capacity supply auction, intended to maintain competitive pricing that’s under threat from a wave of subsidized generation, was approved by the Federal Energy Regulatory Commission on March 9. The rule changes, however, drew the objection of Commissioner Robert Powelson, who argued that the twin goals of ensuring the integrity of the competitive market while accommodating state subsidies is “in conflict and cannot coexist.” Commissioners Cheryl LaFleur and Richard Glick criticized the use of the minimum offer price rule as a standard solution against the impacts of all state policies. New England states, such as Massachusetts, are increasingly backing renewable energy projects to meet climate goals and shift away from fossil fuels in a trend seen undermining the integrity of wholesale markets.

American Electric Power Company Inc.’s wholesale auction held March 6 saw electric capacity for delivery in the 12-months starting June 1 clear at $52.01 per megawatt-hour, falling from the November 2017 price of $52.39. Capacity for delivery over two and three years starting in June cleared at $48.29 per megawatt-hour, and $46.53 per megawatt-hour, respectively. Dayton Power & Light Company’s wholesale auction saw electric capacity for delivery over the two years starting June 1 clear at $48.66 per megawatt-hour, about 4 percent lower than the previous April 2017 auction. The auction results, which were accepted by the Public Utilities Commission of Ohio, determine the default generation rates for utility’s customers. Dayton Power & Light is a unit of AES Corporation.

The Michigan Public Service Commission staff requests that Consumers Energy Co. disclose the renewable generators that have entered the utility’s interconnection queue and contacted Consumers about a supply agreement to determine which projects are next in line to win contracts. The commission has limited Consumers’ obligation to enter into power purchase agreements with small renewable project to the first 150 megawatts in its queue as it investigates the extent of an alleged “glut of unneeded capacity.” Utilities have chafed under the mandate by the Public Utility Regulatory Policies Act that requires them to purchase energy and capacity from small renewable producers at the lower so-called avoided cost rate amid a proliferation of projects.

Public Citizen Inc. continued to press for a federal investigation into $460,000 in ratepayer-funded political contributions by PJM Interconnection LLC, according to comments with the Federal Energy Regulatory Commission on March 12. The Washington-based consumer advocate disputed the credibility of PJM’s claims that the contributions were membership fees for participating in policy summits and were not intended to support any political campaign. The group also reiterated its calls for disclosure of PJM’s broader lobbying spending, underscoring FERC’s position that it’s unlawful to include money for political contributions in regulated rates.

The New Jersey Board of Public Utilities has started reviewing utilities’ response to winter storms Quinn and Riley at the direction of Gov. Phil Murphy, a Democrat, as thousands of residents remain without power, some for more than ten days, according to the board’s March 12 press release. The board will examine whether utilities followed the more than 100 protocols that were implemented following devastating storms that struck the state in 2011 and 2012. The board is planning five public hearings across the state.

The New York Public Service Commission on March 15 approved a three-year plan resetting National Grid’s electric and gas rates from April 1 through March 31, 2021. The commission limited revenue increases in the first year to $43 million for electric customers and $13 million for natural gas customers, lower than the company’s initial request of $326 million and $81 million, respectively. The average electric customer will see monthly bill increases of up to 3.9 percent over the period while a residential natural gas customer will see an increase of up to 4.4 percent. Low-income electric customers will benefit from bill reductions of up to 55 percent. The company said the plan will allow $2.5 billion in investment over three years to modernize electricity and natural gas networks.

The New Hampshire Site Evaluation Committee declined to immediately take up a challenge to its rejection of Eversource Energy’s Northern Pass power line, putting off the appeal process until a later date, according to a March 13 ruling. Eversource is racing to secure all necessary permits to construct the 192-mile U.S.-Canada power line in order for it to maintain a supply contract with Massachusetts. Massachusetts signaled that it will make a final decision on the contract on March 27.

The Federal Energy Regulatory Commission on March 15 granted a request by transmission owners in the Midcontinent Independent System Operator Inc.’s region to waive certain formula rate provisions so that they can incorporate the impacts of the lower federal corporate income tax rate in their 2018 net revenue requirements. The corporate tax rate was reduced to 21 percent from 35 percent effective January 1. The transmission owners said that company-specific formula rate protocols prohibit mid-year adjustments and without the waiver, the tax changes would be implemented in the 2019 rate year, such that customers would not receive the benefits for 2018 until a true-up for that year is completed in 2020.

The Colorado Legislature on March 12 passed bipartisan legislation that would knock down barriers to the use of energy storage batteries by consumers, including through the elimination of unnecessary restrictions or fees. The measure directs state regulators to set up rules for installing the systems and connecting them to the grid. The bill awaits approval by Gov. John Hickenlooper, a Democrat. (SB 18-009)

The West Virginia Department of Environmental Protection ordered Energy Transfer Partners LP to halt construction until a full inspection is undertaken following its failure to provide notification of more than a dozen environmental violations, according to a March 5 order. The 713-mile, $4.2-billion link has incurred dozens of violations and has had operations suspended over failure to comply with rules. Rover is expected to be in full service by the end of the first quarter of 2018, according to a project website.

The Pennsylvania Department of Environmental Protection issued a notice of violation to Sunoco Pipeline LP, a unit of Energy Transfer Partners LP, after drilling fluids from its Mariner East 2 natural gas liquids pipeline were released into a creek in the southeastern part of the state, the third such spill in the area, according to a March 16 filing. The agency said approval is required before the resumption of drilling operations. The pipeline is scheduled to begin full operations by the end of the second quarter, according to the company website.

The U.S. House of Representatives on March 8 passed legislation that would ease emission limits for hazardous air pollutants from plants that generate energy by burning coal refuse. Coal-state lawmakers led by Republican Keith Rothfus, representing Pennsylvania, argue that coal refuse-to-energy plants, which have cleaned up hundreds of tons of coal waste, are at risk of shutting down from stringent environmental standards.

The U.S. Senate passed legislation on March 7 that would foster partnerships between the private-sector and the Energy Department to test and develop advanced nuclear reactors as well as streamline regulatory approvals. Construction of traditional nuclear plants in the U.S. has stalled amid growing competition from cheap natural gas and renewables, throwing the future of the technology into question.

Calpine Corp. suspended an application to build its 255-megawatt Mission Rock Energy Center, citing its inability to participate in Southern California Edison’s procurement program and a broader change in state policies, according to a March 9 filing with the California Energy Commission. The project, a natural gas-fired peaking plant coupled with battery storage, was intended to address local supply shortages on the grid that have emerged with the retirement of 2,000 megawatts of local generating capacity.

U.S. House lawmaker Clay Higgins, a Republican representing Louisiana, introduced legislation on March 13 that would order the U.S. Energy Department to perform demonstration projects for advanced nuclear reactors in a bid to restore the nation’s leadership in developing the technology. Lawmakers and regulators are pursuing next-generation reactors, which are faster and cheaper to build, as larger and costlier nuclear plants have retired amid falling power prices.

U.S. House lawmaker Larry Bucshon, a Republican representing Indiana, introduced legislation on March 14 that would grant tax credits for coal-fired power plants. Over 100,000 megawatts of plant capacity has shut or announced plans to retire since 2010, according to Bucshon, buffeted by low power prices and competition from cheap gas-fired power producers. (H.R. 5270)